What is a SEPA transfer?

You have probably heard of the new SEPA transfer in the news or through your bank. So far, this was not absolutely necessary. Now, however, it will be mandatory from 2014. We'll tell you what it's all about.

What is a SEPA transfer and what is it used for?

The SEPA transfer has been in existence since 2008. As of January 2014, the known euro transfer will finally replace it.

- The SEPA credit transfer standardizes the form and the procedure for transfers of all countries of the European Union and the European Economic Area as well as Switzerland and Moncao.

- The advantage here is that the system is the same for all banks and transfers can therefore arrive within a day. The transfer limit is currently still at 50, 000 euros.

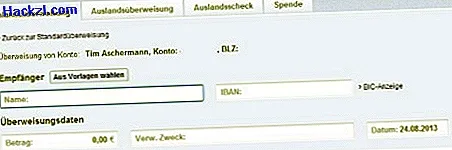

- From 2014, transfers must be carried out both within Germany and within the EU using the IBAN and the BIC. These represent the international equivalent of the account number and sort code.

- As a private individual, however, you can still make transfers with an account number and sort code until 2016. From February 2016 it should only be necessary to enter the IBAN. The BIC is then also superfluous.

- SEPA transfers can only be processed for amounts in euros. For other currencies, you have to make an international transfer.

- Conclusion: With the SEPA transfer, the transfer system is standardized across Europe. This reduces the effort and transfers arrive faster at the recipient. So it's best to get used to your IBAN and BIC right now. If you like, you can stay with your account number and sort code until 2016.

This practical tip tells you what to look out for when transferring money to the EU and the rest of the world.